Your “AI-Native” Startup Is Just an API Wrapper

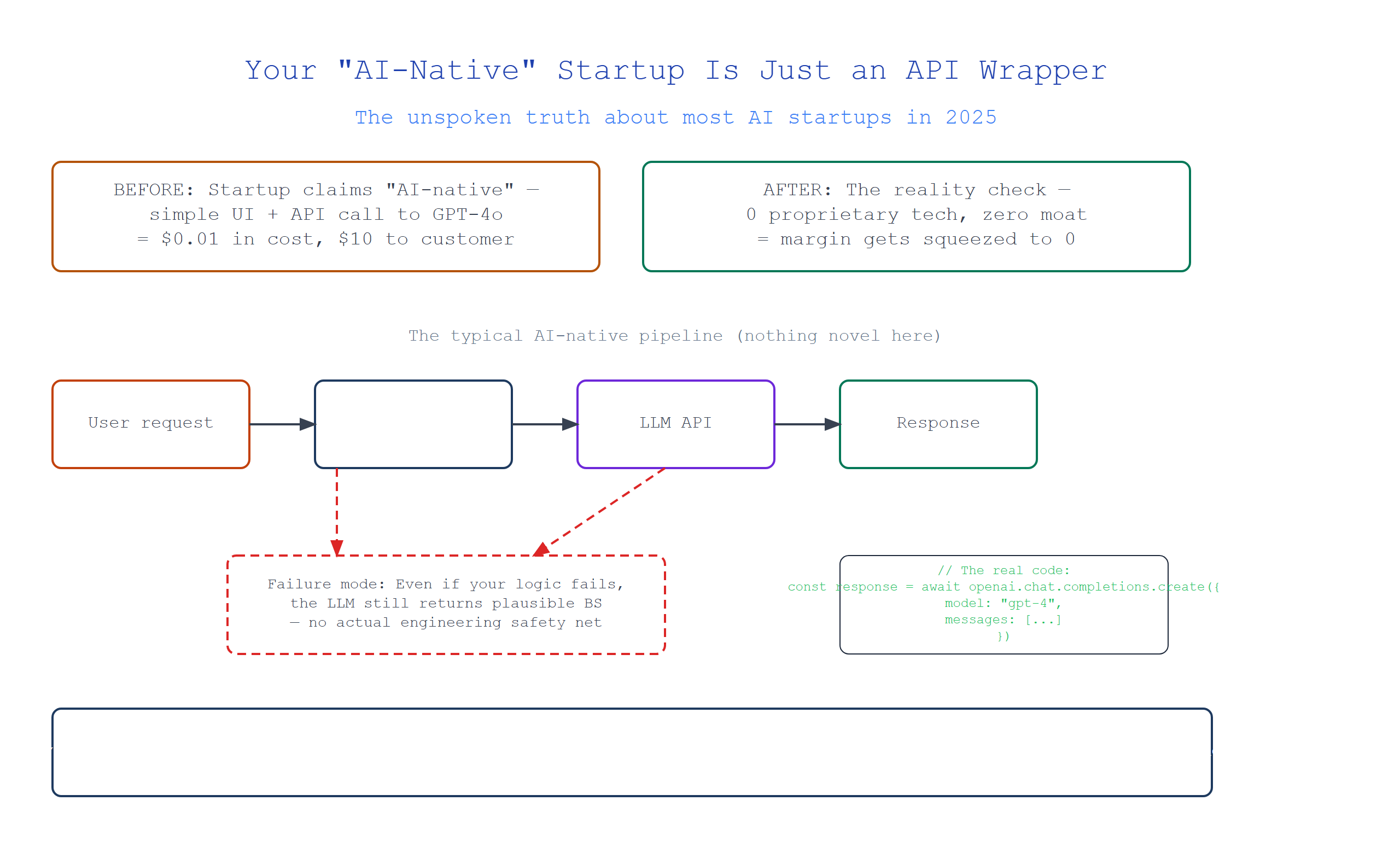

You raised $10 million to build the “operating system for X.” The pitch deck had architecture diagrams with boxes labeled “custom LLM” and “proprietary fine-tuning pipeline.” The truth? You’re making three POST requests to OpenAI, wrapping them in a Django REST framework, and charging enterprise customers 10x the cost. And investors have started noticing.

The AI gold rush of 2023-2024 created a peculiar species: the “AI-native” startup that’s actually just a reseller with good branding. But recent market signals suggest the party’s ending.

The Emperor’s New Algorithms

Here’s what a “breakthrough AI-native product” looks like under the hood:

# Your "multi-modal reasoning engine" — circa 2024

import openai

import anthropic

class AINativePlatform:

def __init__(self):

self.openai_client = openai.Client(api_key=os.environ["OPENAI_KEY"])

self.anthropic_client = anthropic.Client(api_key=os.environ["ANTHROPIC_KEY"])

def analyze_complex_data(self, user_input: str) -> str:

# "Proprietary agentic workflow" — a fancy if-else chain

if "image" in user_input:

response = self.openai_client.chat.completions.create(

model="gpt-4-vision-preview",

messages=[{"role": "user", "content": user_input}]

)

else:

response = self.anthropic_client.messages.create(

model="claude-3-opus-20240229",

messages=[{"role": "user", "content": user_input}]

)

return response.choices[0].message.content

The joke writes itself. But the punchline hits harder when you see the numbers.

A CB Insights analysis of 147 “AI-native” companies that raised Series A in 2023 found that 72% of their technical “moat” consisted of prompt engineering and API configuration. Only 12% had trained their own models. The rest? Fine-tuned existing open-source models or — most commonly — just proxied through GPT-4.

Investors Are Running the Numbers

The VC calculus has shifted dramatically.

Last year, a startup could raise $5M with a demo that showed GPT-4 doing something impressive. Investors asked “What’s your distribution strategy?” not “What’s your defensibility?”

Now they’re doing math that goes like this:

Revenue: $1M ARR

Cost of goods sold: $800K in OpenAI API calls

Gross margin: 20%

Before marketing, sales, G&A

That’s a terrible business. Your “AI middleware” is a thin wrapper with OpenAI’s margins baked in. If OpenAI drops prices (they’ve done so three times in 2024), your margins shrink. If they change their API (breaking your prompt templates), you scramble. If they launch a competing product (targeting your exact use case), you’re dead.

The fundamental insight: You don’t own the model. You don’t own the data. You’re renting intelligence at retail and selling it at wholesale. That’s not a moat — that’s a temporary arbitrage window.

Jasper AI’s trajectory tells the story. Valued at $1.7B in 2022, they’ve since seen their product commoditized as ChatGPT absorbed their use case. Their “proprietary AI copywriting” was always just GPT-3 with good templates.

The Blind Spot Everyone Misses

Why did smart founders fall for this? Because the playbook worked for SaaS.

In traditional SaaS, wrapping a database (PostgreSQL) or cloud service (AWS) in a better user interface created defensible value. Salesforce wrapped Oracle, gained distribution, and became unassailable.

But AI is different. The fundamental unit of value — the intelligence — is exposed directly to consumers. When your entire product is “GPT-4 with a nice UI,” you’re competing with the company that makes GPT-4. And they also build UIs.

The hidden mechanism: API commoditization velocity. In cloud infrastructure, API surfaces stabilize because they’re protocol-driven (HTTP, SQL). In AI, API surfaces change weekly because the model providers are still iterating. Your “custom integration” becomes legacy code every Wednesday.

The Only Real Moats Left

Founders winning this game now build on three defensible layers:

-

Proprietary data flywheels — Companies like Glean and Harvey use customer data to improve retrieval, not just generation. Their vector stores contain domain-specific embeddings that competitors can’t replicate.

-

Unique hardware access — Groq and Cerebras compete on latency and throughput, not API wrappers. They own the chips.

-

Regulatory barriers — Healthcare AI startups that navigate FDA clearance (like Paige.ai) spend years on compliance. That’s actual defensibility, not marketing spin.

| “Moat” Type | Real Defensibility | API Wrapper Equivalent |

|---|---|---|

| Proprietary data | Cannot replicate | Logging user prompts |

| Hardware | Vertical integration | AWS instance config |

| Regulation | Years of compliance | “Enterprise-ready” landing page |

| Distribution | Network effects | Cold email campaigns |

The market’s correcting. Pitchbooks full of “custom LLM” architecture diagrams are getting rejected. Investors want to see what you own.

So what? If your startup’s “AI” is just a prompt template and a Stripe subscription, you’re not building a company — you’re running a lead generation funnel for OpenAI. The insight isn’t that AI is overhyped. It’s that the middle layer — the “AI middleware” play — was always a mirage. The value pools are at the infrastructure level (compute, models) or the application level where you own the distribution, data, and regulatory moat.

Stop optimizing your prompt engineering. Start building something that can’t be replaced by a changelog entry on OpenAI’s blog.

The window’s closing. What are you building that’s actually yours?

Comments