Your 100% S&P 500 Portfolio Isn’t Ready for the AI IPO Earthquake

You saved $35,000. You did the smart, boring thing. You put it all into VOO, the Vanguard S&P 500 ETF. Every finance guru told you this was the easy button. Buy the whole market. Don’t think about it again.

Then you started reading the news. OpenAI. Anthropic. SpaceX. Words like “trillion-dollar IPO” started showing up in your feed. And a small, nagging voice in your head asked a scary question: what happens to my $35,000 if this AI bubble pops?

You are not crazy for asking. You are being a smart investor. Let’s walk through this together, slowly, like a mentor sitting next to you with a cup of coffee. No big words. No scary jargon. Just clear thinking, real numbers, and a plan you can actually follow.

Part 1: The Problem With the Basket

1. What Does “Market-Cap Weighted” Even Mean?

Picture a giant fruit basket. This basket is supposed to hold a little bit of everything — strawberries, grapes, apples, bananas, watermelons. That sounds balanced, right? A bit of this, a bit of that.

But here’s the catch. This basket doesn’t give every fruit equal space. It gives each fruit space based on how much it weighs. A watermelon weighs as much as fifty strawberries. So the basket fills up with watermelons first. The strawberries get squished into a tiny corner, barely visible, easy to ignore.

That is exactly how VOO works. VOO is a “market-cap weighted” fund. That fancy phrase just means: the bigger the company, the more of your money goes into it. VOO holds about 500 companies. But it does not give each company an equal slice. The biggest companies — the watermelons — get huge slices. The smaller companies — the strawberries — get crumbs.

So when people say “VOO is diversified,” that is only half true. Yes, you own a piece of 500 companies. But a handful of giant companies control most of the weight. You are not eating a balanced fruit salad. You are mostly eating watermelon, with a sprinkle of everything else on top.

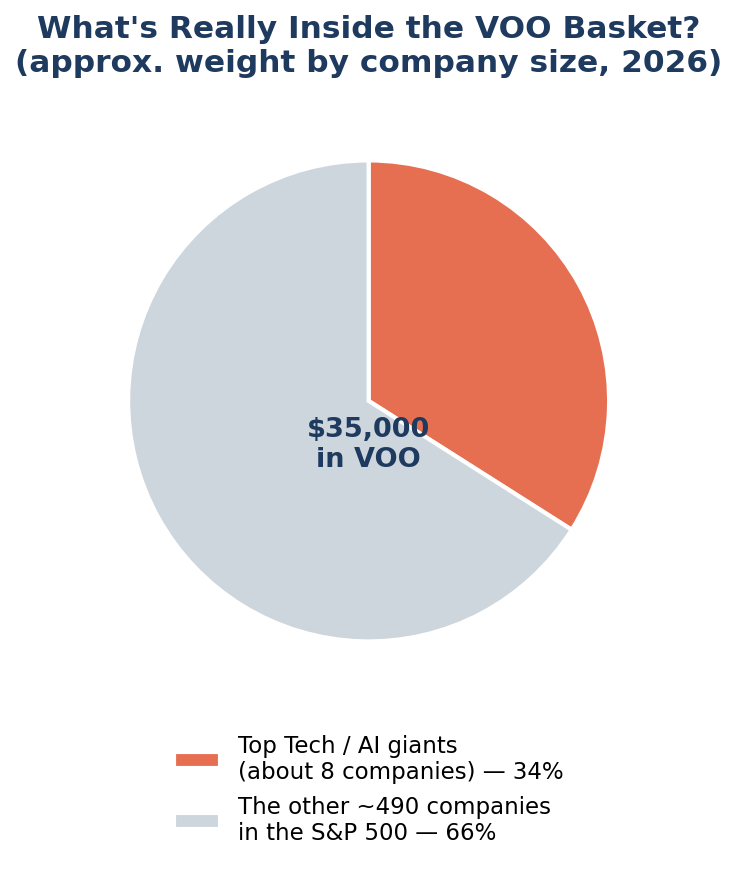

2. How Much of Your Basket Is Already Tech?

Here is the part that should make you sit up. Right now, roughly one-third of VOO’s value comes from just a small handful of giant technology and AI-linked companies — names like Microsoft, Apple, Nvidia, Amazon, Alphabet (Google’s parent), and Meta. About eight companies. Out of nearly 500.

Think about that for a second. When you bought VOO, you probably thought: “Great, I now own a tiny piece of 500 different companies. I’m spread out. I’m safe.” But in reality, more than thirty cents of every dollar you invested is riding on the success of a tiny cluster of tech giants. If you put $35,000 into VOO, roughly $11,900 of it is already a concentrated bet on Big Tech and AI — whether you meant to make that bet or not.

That’s not “diversified” in the way most beginners imagine. That’s a fruit basket that is secretly mostly watermelon.

3. The AI IPO Wave Will Make This Basket Even Heavier

Now here comes the twist that worries you, and honestly, it should get your attention.

When a giant private company — like OpenAI, Anthropic, or SpaceX — finally sells shares to the public for the first time (an “IPO,” which just means “Initial Public Offering,” or in plain English: “the day a company starts selling pieces of itself on the stock market”), it can become enormous overnight. If that company grows big enough, it gets added to the S&P 500 index — the list of companies VOO is built to copy.

Here’s the key part: VOO doesn’t get to choose. It’s not run by a person who picks favorites. It’s run by a formula. The formula says, “If a company is big enough to join the S&P 500, you must buy it, and you must buy it in proportion to its size.” VOO is like a basket on an automatic conveyor belt. Whatever giant new fruit rolls onto the belt, the basket must make room for it — usually by giving it one of the biggest slots.

So picture this chain of events:

- A massive AI company goes public and is worth hundreds of billions of dollars on day one.

- It gets added to the S&P 500.

- VOO is automatically forced to buy huge amounts of it — using your money.

- Your “balanced fruit basket” becomes even more lopsided toward AI and tech than it already is.

Now imagine the second half of that story: the AI bubble bursts. Maybe the new AI companies don’t make the profits investors hoped for. Maybe the hype cools off faster than the technology can catch up. When that happens, the giant slices of your basket — the ones stuffed with AI and tech — could lose value fast. And because those slices make up such a big chunk of VOO, your whole basket falls hard, even though you thought you were “spread out.”

This is the real risk. It’s not that VOO is a bad fund. It’s that VOO is quietly becoming a bigger and bigger bet on one industry, and you didn’t get a vote.

Part 2: Meet Your Five Defensive Players

So if VOO is leaning harder into tech every year, what can you do? You don’t have to abandon the stock market. You just need to bring in some teammates who play a different position — ones who don’t rise and fall with AI headlines.

Think of these five funds as shields. Each one is a basket of companies that make their money in a different, steadier way. Here they are, with friendly nicknames so they’re easy to remember.

1. XLP — “The Grocery Cart Fund” (Consumer Staples)

What it owns: Companies that make the stuff you buy no matter what — toothpaste, soap, shampoo, toilet paper, soda, snacks. Think Procter & Gamble, Coca-Cola, Walmart, Costco.

How it shields you: People don’t stop brushing their teeth during a recession. They don’t stop buying groceries because an AI company’s stock dropped. This fund’s companies sell things people need, not things people only want. When tech stocks wobble, grocery-cart companies usually keep humming along, because life — and shopping carts — keep rolling no matter what’s happening on Wall Street.

2. XLU — “The Light Switch Fund” (Utilities)

What it owns: Companies that supply electricity, water, and natural gas to homes and businesses.

How it shields you: You’re going to flip your light switch tonight whether the stock market is up or down. You’re going to run your dishwasher. You’re going to charge your phone. These companies get paid steady, predictable amounts every single month, almost like a subscription that never gets canceled. That steadiness makes them act like a calm anchor when flashy tech stocks are bouncing around like a rollercoaster.

3. XLV — “The Doctor’s Office Fund” (Healthcare)

What it owns: Companies that make medicine, run hospitals, build medical devices, and develop new treatments. Think Johnson & Johnson, UnitedHealth, Eli Lilly.

How it shields you: Getting sick doesn’t check the stock market first. People need medicine and doctors in good times and bad times. This makes healthcare spending one of the steadiest forces in the economy. While an AI company’s value can swing wildly based on a single headline, a hospital still treats patients and a drug company still sells medicine — rain or shine, boom or bust.

4. DFUS — “The Whole Neighborhood Fund” (Dimensional U.S. Equity Market ETF)

What it owns: A very wide mix of U.S. companies — big ones, medium ones, and smaller ones — chosen with extra attention to companies that look like good long-term value, not just the biggest names of the moment.

How it shields you: Remember our fruit basket problem — a few watermelons crushing the strawberries? This fund is built to fix exactly that. It deliberately gives more room to smaller, steadier companies instead of stacking everything on a handful of giants. That means your money isn’t riding on the same small group of tech superstars that VOO leans on so heavily. It’s more like a basket that was packed by someone who actually measured each fruit instead of just grabbing the biggest ones first.

5. RSP — “The Everyone-Gets-A-Trophy Fund” (Equal-Weight S&P 500 ETF)

What it owns: The exact same 500 companies as VOO — but here’s the twist — it gives each one roughly the same size slice, instead of letting the giants dominate.

How it shields you: This is the cleanest fix to the watermelon problem. Imagine the same fruit basket, but now a fair referee steps in and says, “Nope — every fruit gets an equal-sized spot, no matter how much it weighs.” Suddenly, the strawberries matter just as much as the watermelons. If a few giant tech companies stumble, this fund doesn’t fall nearly as hard, because they were never allowed to take over the whole basket in the first place.

Part 3: The 3-Year Simulation Arena

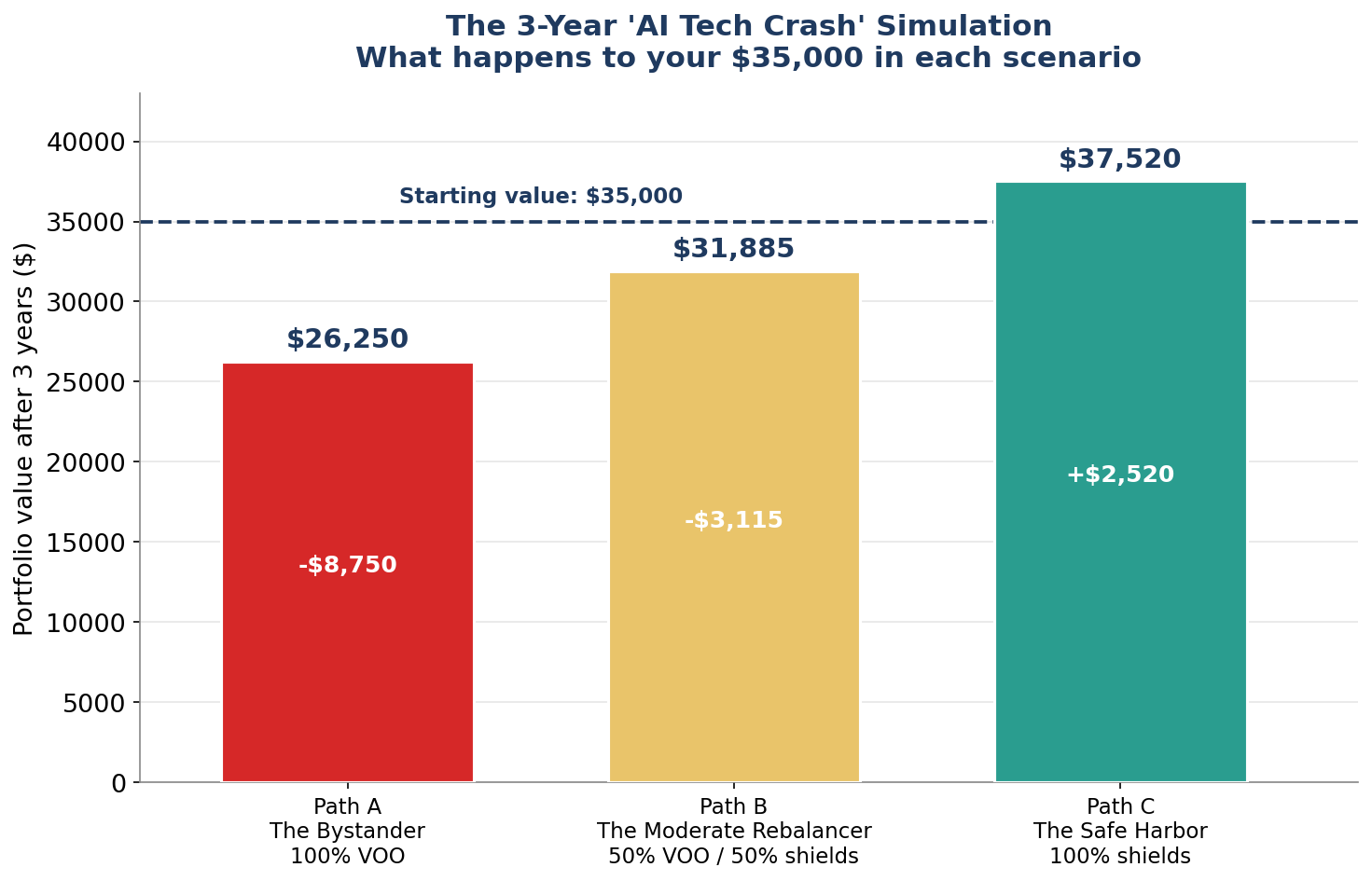

Okay — time for the fun part. Let’s run an experiment. Let’s imagine a believable, scary scenario: an “AI Tech Crash.” Over the next three years, the excitement around AI cools off. New AI companies don’t deliver the profits people expected. Tech stocks slide hard, and because VOO is so loaded with tech, VOO loses 25% of its value over those three years.

Meanwhile, our five defensive shields — XLP, XLU, XLV, DFUS, and RSP — do what shields are supposed to do. They don’t shoot to the moon, but they hold up far better, because they aren’t riding the AI rollercoaster. (For this simulation, we’ll imagine modest, realistic results for each: XLP +12%, XLU +9%, XLV +15%, DFUS +5%, and RSP -5% — since RSP still owns some tech, just in smaller doses, it dips a little, but nowhere near as much as VOO.)

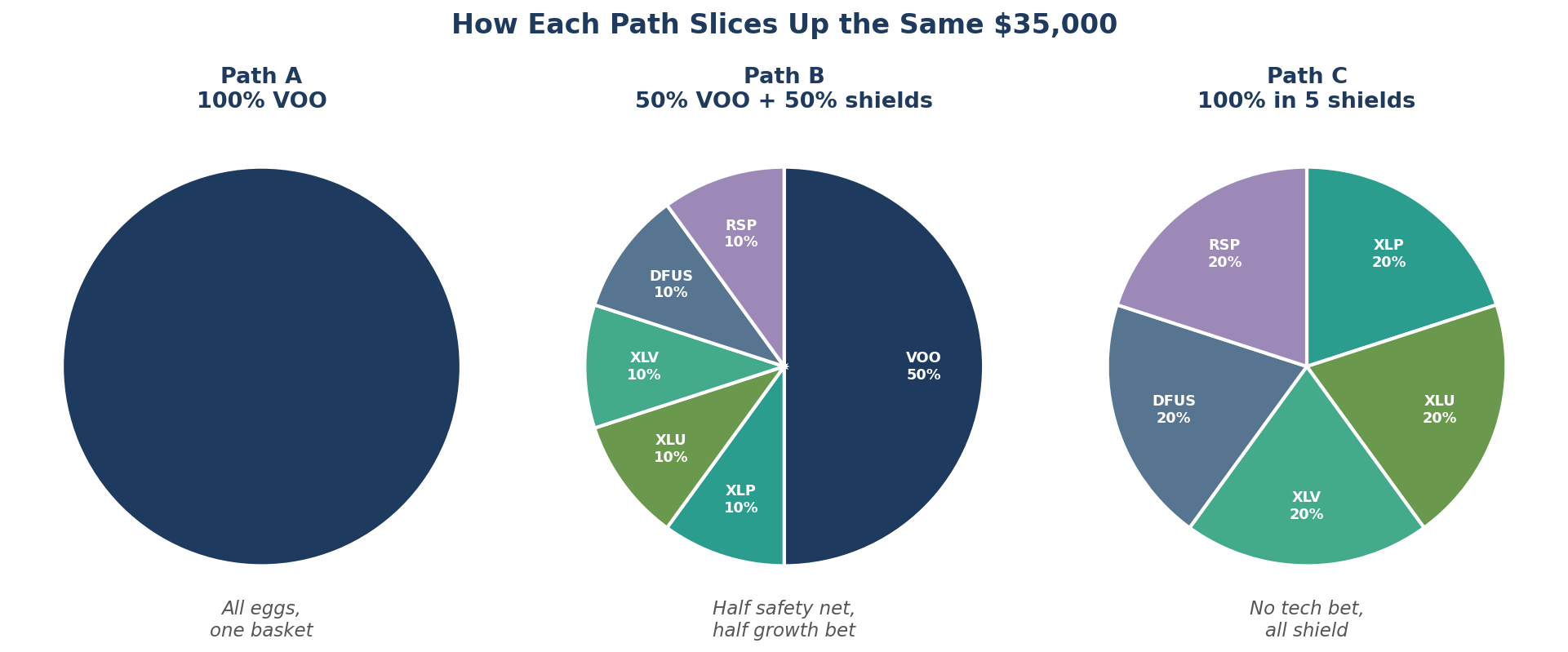

Now let’s follow three different investors, each starting with the exact same $35,000, each making a different choice.

- Path A — The Bystander: Keeps 100% of the money in VOO. Does nothing. Rides it out.

- Path B — The Moderate Rebalancer: Splits the money in half — 50% stays in VOO, and the other 50% gets divided evenly across the five shield funds (10% each).

- Path C — The Safe Harbor: Moves all the money out of VOO and spreads it evenly across the five shield funds (20% each).

Here’s how the three years play out:

| Path | Starting Value | Final Value (after 3 years) | Total Dollars Lost (or Gained) |

|---|---|---|---|

| A — The Bystander (100% VOO) | $35,000 | $26,250 | −$8,750 |

| B — The Moderate Rebalancer (50% VOO / 50% shields) | $35,000 | $31,885 | −$3,115 |

| C — The Safe Harbor (100% shields) | $35,000 | $37,520 | +$2,520 |

Look closely at what just happened. The Bystander lost nearly $9,000 — about a quarter of everything they had — because every dollar was riding the same wave. The Moderate Rebalancer also felt the dip, but the shields softened the blow by more than half, cutting the damage down to about $3,100. And The Safe Harbor investor didn’t just avoid the crash — because their money wasn’t tied to the AI rollercoaster at all, they actually finished above where they started, up about $2,500.

Now, a quick and important word of honesty: this is a simulation, not a prediction. Nobody — not your mentor, not a fancy fund manager, not a robot — can know exactly what the market will do. Real markets zig and zag in ways nobody can perfectly guess. But this exercise isn’t about predicting the future. It’s about seeing, in plain numbers, why putting all your eggs in one fast-moving basket can hurt so much more than spreading them out. That’s the whole point of a shield — you don’t need to know exactly when the storm will hit. You just need to be wearing one before it does.

Part 4: The Mentor’s Step-by-Step Action Plan

You’ve seen the problem. You’ve met the shields. You’ve watched the simulation play out. Now, let’s turn all of that into a calm, simple plan — the kind of plan a patient mentor would scribble on a napkin for you over coffee.

Step 1: Don’t panic-sell everything tomorrow

Big, sudden moves are where beginners get hurt the most. Selling everything in one click feels powerful in the moment, but it can quietly cost you in two ways: you might lock in a loss right before the market turns around, and you might trigger something called a taxable event.

Here’s what that means in plain English: when you sell an investment for more than you paid for it, the government usually wants a small slice of that profit — that’s a “capital gain,” and it can mean a tax bill. When you sell for less than you paid, that’s a “loss,” which can sometimes actually help you at tax time. The lesson here isn’t “never sell.” It’s “know what selling triggers, so you’re not surprised by a tax bill next spring.” If your $35,000 has grown over time, selling it all at once could mean owing taxes on those gains — so it’s worth thinking this through, and even asking a tax professional, before you make one big move.

Step 2: Shift gradually, like filling a bathtub drop by drop

You don’t have to choose between “do nothing” and “sell everything today.” There’s a gentle middle path, and it has a friendly name: Dollar-Cost Averaging, or DCA for short. All that fancy term means is this — instead of moving all your money at once, you move a small piece on a regular schedule. For example, you might shift one-twelfth of your goal amount every month for a year.

Why does this help? Because nobody can perfectly time the market — not you, not the experts. By spreading your moves out over many months, you avoid the stress of guessing “is today the right day?” Some months you’ll move money when prices are a little higher, some months when they’re a little lower, and over time it tends to even out. It feels less like jumping off a diving board and more like wading into a pool, one calm step at a time.

And here’s a handy little tool that makes this even easier for beginners: fractional shares. In the old days, if a share of a fund cost $400, you needed $400 to buy even one. Today, most brokerages let you buy a slice of a share — like buying $50 worth of a fund, even if one full share costs $400. This means you don’t need a big lump sum to start shifting your money around. You can move exactly the amount you’re comfortable with, whenever you’re ready, without waiting to save up for a “whole” share.

Step 3: Ask yourself these three questions before you click “sell”

Before making any big change, sit down somewhere quiet and honestly answer these three questions. They’re not trick questions — they’re a mirror.

-

“If my portfolio dropped 25% tomorrow, would I lose sleep over it — or would I shrug and wait it out?” Your honest answer tells you how much of a shield you actually need. If the thought makes your stomach drop, that’s useful information, not weakness.

-

“Am I investing money I’ll need soon, or money I won’t touch for many years?” Money you need next year for a big expense should generally be handled far more carefully than money you won’t touch for ten or twenty years. The longer your money can sit and grow, the more bumps in the road it can usually ride out.

-

“Am I making this change because I’ve thought it through calmly — or because I’m scared of a headline I read this morning?” There’s a big difference between a thoughtful plan and a panic reaction. A plan you can explain calmly, in your own words, to a friend, is usually a much better guide than a gut reaction to a scary news story.

Putting it all together

There’s no single “correct” answer here — Path A, B, and C aren’t a multiple-choice quiz with one right circle. They’re three honest examples of how different comfort levels can lead to very different outcomes. A 25-year-old with decades ahead of them might comfortably stay closer to Path A or B. Someone closer to needing their money, or someone who simply sleeps better with more balance, might lean toward Path B or C.

The real win here isn’t picking the “perfect” portfolio. It’s understanding why your basket looks the way it does, what could shake it, and how you can calmly add a few shields — at your own pace, on your own schedule — so that whatever the AI IPO wave brings, you’re not caught off guard. That’s not fear talking. That’s what being a thoughtful investor actually looks like.

Comments